library(nabla)

#>

#> Attaching package: 'nabla'

#> The following objects are masked from 'package:stats':

#>

#> D, derivIntroduction

The gradient() and hessian() functions in

nabla return plain numeric vectors and

matrices — exactly what R’s built-in optimizers expect. This

vignette shows how to plug AD derivatives into optim() and

nlminb() for optimization.

The integration pattern:

# optim() with AD gradient

optim(start, fn = nll, gr = ngr, method = "BFGS")

# nlminb() with AD gradient + Hessian

nlminb(start, objective = nll, gradient = ngr, hessian = nhess)Sign convention: Both optim() and

nlminb() minimize. For maximization (e.g.,

MLE), negate everything:

fn = function(x) -f(x)gr = function(x) -gradient(f, x)hessian = function(x) -hessian(f, x)

Key difference between optimizers:

optim() |

nlminb() |

|

|---|---|---|

| Gradient function |

gr argument (used during optimization) |

gradient argument |

| Hessian function | Not supported — hessian=TRUE only computes it

after convergence |

hessian argument (used during optimization) |

| Best use | BFGS with AD gradient | Full second-order optimization |

optim() with AD gradients

Let’s fit a

Normal(,

)

model using optim(). First, define the log-likelihood with

sufficient statistics:

set.seed(42)

data_norm <- rnorm(100, mean = 5, sd = 2)

n <- length(data_norm)

sum_x <- sum(data_norm)

sum_x2 <- sum(data_norm^2)

ll_normal <- function(x) {

mu <- x[1]

sigma <- exp(x[2]) # unconstrained: x[2] = log(sigma)

-n * log(sigma) - (1 / (2 * sigma^2)) * (sum_x2 - 2 * mu * sum_x + n * mu^2)

}Reparameterization. Because

,

we optimize over

so that the parameter space is fully unconstrained — a standard practice

in optimization. Without this, BFGS can step

through zero, producing NaN from log(sigma)

and causing divergence. The AD chain rule propagates through

exp() automatically, so gradient() and

hessian() return derivatives with respect to

without any manual Jacobian adjustment.

Now compare BFGS with and without the AD gradient:

# Negated versions for minimization

nll <- function(x) -ll_normal(x)

ngr <- function(x) -gradient(ll_normal, x)

# Starting value: mu = 0, log(sigma) = 0 (i.e., sigma = 1)

start <- c(0, 0)

# Without gradient: optim uses internal finite differences

fit_no_gr <- optim(start, fn = nll, method = "BFGS")

# With AD gradient

fit_ad_gr <- optim(start, fn = nll, gr = ngr, method = "BFGS")

# Compare (transform x[2] back to sigma for display)

data.frame(

method = c("BFGS (no gradient)", "BFGS (AD gradient)"),

mu = c(fit_no_gr$par[1], fit_ad_gr$par[1]),

sigma = exp(c(fit_no_gr$par[2], fit_ad_gr$par[2])),

fn_calls = c(fit_no_gr$counts["function"], fit_ad_gr$counts["function"]),

gr_calls = c(fit_no_gr$counts["gradient"], fit_ad_gr$counts["gradient"]),

convergence = c(fit_no_gr$convergence, fit_ad_gr$convergence)

)

#> method mu sigma fn_calls gr_calls convergence

#> 1 BFGS (no gradient) 5.065079 2.072403 39 16 0

#> 2 BFGS (AD gradient) 5.065088 2.072401 39 16 0Both reach the same optimum, but the AD gradient version typically uses fewer function evaluations because it has exact gradient information.

# Verify against analytical MLE

mle_mu <- mean(data_norm)

mle_sigma <- sqrt(mean((data_norm - mle_mu)^2))

cat("Analytical MLE: mu =", round(mle_mu, 6), " sigma =", round(mle_sigma, 6), "\n")

#> Analytical MLE: mu = 5.06503 sigma = 2.072274

cat("optim+AD MLE: mu =", round(fit_ad_gr$par[1], 6),

" sigma =", round(exp(fit_ad_gr$par[2]), 6), "\n")

#> optim+AD MLE: mu = 5.065088 sigma = 2.072401

nlminb() with AD gradient + Hessian

nlminb() is the only base R optimizer that accepts a

Hessian function argument, making it the natural target

for second-order AD:

nhess <- function(x) -hessian(ll_normal, x)

fit_nlminb <- nlminb(start,

objective = nll,

gradient = ngr,

hessian = nhess)

cat("nlminb MLE: mu =", round(fit_nlminb$par[1], 6),

" sigma =", round(exp(fit_nlminb$par[2]), 6), "\n")

#> nlminb MLE: mu = 5.06503 sigma = 2.072274

cat("Converged:", fit_nlminb$convergence == 0, "\n")

#> Converged: TRUE

cat("Iterations:", fit_nlminb$iterations, "\n")

#> Iterations: 8

cat("Function evaluations:", fit_nlminb$evaluations["function"], "\n")

#> Function evaluations: 10

cat("Gradient evaluations:", fit_nlminb$evaluations["gradient"], "\n")

#> Gradient evaluations: 9With exact Hessian information, nlminb() can achieve

faster convergence than quasi-Newton methods (like BFGS) that

approximate the Hessian from gradient history.

Logistic regression example

To demonstrate multi-parameter optimization, let’s fit a logistic

regression and compare with R’s glm():

# Simulate data

set.seed(7)

n_lr <- 200

x1 <- rnorm(n_lr)

x2 <- rnorm(n_lr)

X <- cbind(1, x1, x2)

beta_true <- c(-0.5, 1.2, -0.8)

eta_true <- X %*% beta_true

prob_true <- 1 / (1 + exp(-eta_true))

y <- rbinom(n_lr, 1, prob_true)

# Log-likelihood for nabla

ll_logistic <- function(x) {

result <- dual_constant(0)

for (i in seq_len(n_lr)) {

eta_i <- x[1] * X[i, 1] + x[2] * X[i, 2] + x[3] * X[i, 3]

result <- result + y[i] * eta_i - log(1 + exp(eta_i))

}

result

}

# Numeric version for optim's fn

ll_logistic_num <- function(beta) {

eta <- X %*% beta

sum(y * eta - log(1 + exp(eta)))

}Fit with optim() using the AD gradient:

nll_lr <- function(x) -ll_logistic_num(x)

ngr_lr <- function(x) -gradient(ll_logistic, x)

fit_lr <- optim(c(0, 0, 0), fn = nll_lr, gr = ngr_lr, method = "BFGS")Compare with glm():

fit_glm <- glm(y ~ x1 + x2, family = binomial)

# Coefficient comparison

data.frame(

parameter = c("Intercept", "x1", "x2"),

optim_AD = round(fit_lr$par, 6),

glm = round(coef(fit_glm), 6),

difference = round(fit_lr$par - coef(fit_glm), 10)

)

#> parameter optim_AD glm difference

#> (Intercept) Intercept -0.703586 -0.703587 1.5805e-06

#> x1 x1 1.345038 1.345043 -5.7000e-06

#> x2 x2 -0.881894 -0.881896 2.3194e-06The AD-based optimizer recovers the same coefficients as

glm().

Standard errors from the Hessian

After optimization, the observed information matrix (negative Hessian at the optimum) provides the asymptotic variance-covariance matrix:

# Observed information at the optimum (negative Hessian)

obs_info <- -hessian(ll_logistic, fit_lr$par)

# Variance-covariance matrix

vcov_ad <- solve(obs_info)

# Standard errors

se_ad <- sqrt(diag(vcov_ad))

# Compare with glm's standard errors

se_glm <- summary(fit_glm)$coefficients[, "Std. Error"]

data.frame(

parameter = c("Intercept", "x1", "x2"),

SE_AD = round(se_ad, 6),

SE_glm = round(se_glm, 6),

ratio = round(se_ad / se_glm, 8)

)

#> parameter SE_AD SE_glm ratio

#> (Intercept) Intercept 0.186306 0.186293 1.000069

#> x1 x1 0.228300 0.228277 1.000101

#> x2 x2 0.188825 0.188810 1.000077The standard errors from AD’s exact Hessian match

glm()’s Fisher-scoring estimates closely (the ratio should

be very near 1.0).

Convergence comparison

Let’s compare how many iterations each optimizer strategy needs by tracking the negative log-likelihood at each step:

# Track convergence for three methods on the Normal(mu, sigma) model

# We'll use a callback-style approach via optim's trace

# Method 1: Nelder-Mead (no gradient)

fit_nm <- optim(start, fn = nll, method = "Nelder-Mead",

control = list(maxit = 200))

# Method 2: BFGS with AD gradient

fit_bfgs <- optim(start, fn = nll, gr = ngr, method = "BFGS")

# Method 3: nlminb with AD gradient + Hessian

fit_nlm <- nlminb(start, objective = nll, gradient = ngr, hessian = nhess)

# Summary comparison

data.frame(

method = c("Nelder-Mead", "BFGS + AD grad", "nlminb + AD grad+hess"),

fn_evals = c(fit_nm$counts["function"],

fit_bfgs$counts["function"],

fit_nlm$evaluations["function"]),

converged = c(fit_nm$convergence == 0,

fit_bfgs$convergence == 0,

fit_nlm$convergence == 0),

nll = c(fit_nm$value, fit_bfgs$value, fit_nlm$objective)

)

#> method fn_evals converged nll

#> 1 Nelder-Mead 99 TRUE 122.8647

#> 2 BFGS + AD grad 39 TRUE 122.8647

#> 3 nlminb + AD grad+hess 10 TRUE 122.8647

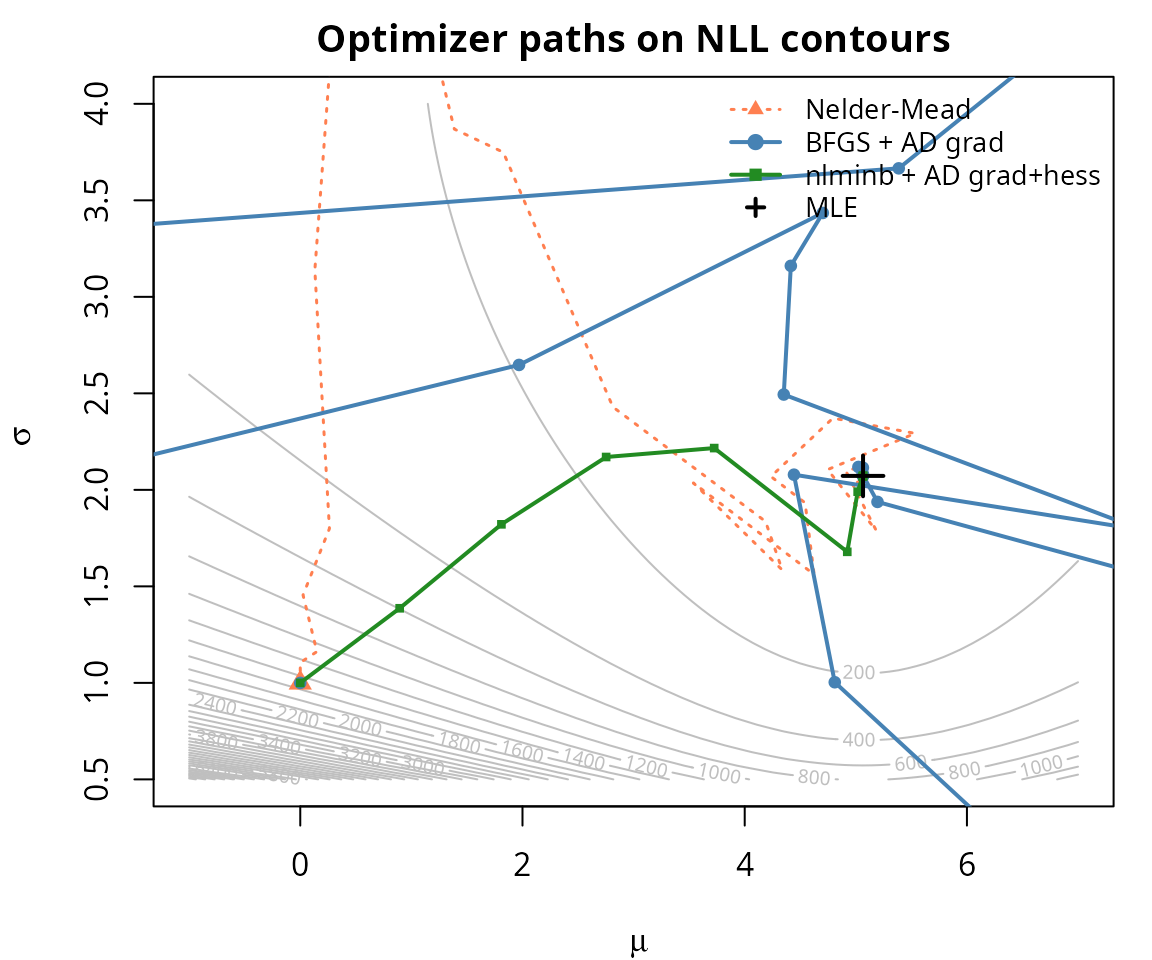

# Contour plot with optimizer paths

# Recompute paths by running each optimizer and collecting iterates

# Helper: collect iterates via BFGS

bfgs_trace <- list()

bfgs_nll <- function(x) {

bfgs_trace[[length(bfgs_trace) + 1L]] <<- x

-ll_normal(x)

}

bfgs_trace <- list()

optim(start, fn = bfgs_nll, gr = ngr, method = "BFGS")

#> $par

#> [1] 5.0650877 0.7287078

#>

#> $value

#> [1] 122.8647

#>

#> $counts

#> function gradient

#> 39 16

#>

#> $convergence

#> [1] 0

#>

#> $message

#> NULL

bfgs_path <- do.call(rbind, bfgs_trace)

# Helper: collect iterates via Nelder-Mead

nm_trace <- list()

nm_nll <- function(x) {

nm_trace[[length(nm_trace) + 1L]] <<- x

-ll_normal(x)

}

nm_trace <- list()

optim(start, fn = nm_nll, method = "Nelder-Mead",

control = list(maxit = 200))

#> $par

#> [1] 5.0655326 0.7286854

#>

#> $value

#> [1] 122.8647

#>

#> $counts

#> function gradient

#> 99 NA

#>

#> $convergence

#> [1] 0

#>

#> $message

#> NULL

nm_path <- do.call(rbind, nm_trace)

# Helper: collect iterates via nlminb

nlm_trace <- list()

nlm_nll <- function(x) {

nlm_trace[[length(nlm_trace) + 1L]] <<- x

-ll_normal(x)

}

nlm_trace <- list()

nlminb(start, objective = nlm_nll, gradient = ngr, hessian = nhess)

#> $par

#> [1] 5.0650296 0.7286466

#>

#> $objective

#> [1] 122.8647

#>

#> $convergence

#> [1] 0

#>

#> $iterations

#> [1] 8

#>

#> $evaluations

#> function gradient

#> 10 9

#>

#> $message

#> [1] "relative convergence (4)"

nlm_path <- do.call(rbind, nlm_trace)

# Build contour grid

mu_grid <- seq(-1, 7, length.out = 100)

sigma_grid <- seq(0.5, 4, length.out = 100)

nll_surface <- outer(mu_grid, sigma_grid, Vectorize(function(m, s) {

-ll_normal(c(m, log(s)))

}))

# Transform paths from (mu, log_sigma) to (mu, sigma) for plotting

bfgs_path[, 2] <- exp(bfgs_path[, 2])

nm_path[, 2] <- exp(nm_path[, 2])

nlm_path[, 2] <- exp(nlm_path[, 2])

par(mar = c(4, 4, 2, 1))

contour(mu_grid, sigma_grid, nll_surface, nlevels = 30,

xlab = expression(mu), ylab = expression(sigma),

main = "Optimizer paths on NLL contours",

col = "grey75")

# Nelder-Mead path (subsample for clarity)

nm_sub <- nm_path[seq(1, nrow(nm_path), length.out = min(50, nrow(nm_path))), ]

lines(nm_sub[, 1], nm_sub[, 2], col = "coral", lwd = 1.5, lty = 3)

points(nm_sub[1, 1], nm_sub[1, 2], pch = 17, col = "coral", cex = 1.2)

# BFGS path

lines(bfgs_path[, 1], bfgs_path[, 2], col = "steelblue", lwd = 2, type = "o",

pch = 19, cex = 0.6)

# nlminb path

lines(nlm_path[, 1], nlm_path[, 2], col = "forestgreen", lwd = 2, type = "o",

pch = 15, cex = 0.6)

# MLE

points(mle_mu, mle_sigma, pch = 3, col = "black", cex = 2, lwd = 2)

legend("topright",

legend = c("Nelder-Mead", "BFGS + AD grad", "nlminb + AD grad+hess", "MLE"),

col = c("coral", "steelblue", "forestgreen", "black"),

lty = c(3, 1, 1, NA), pch = c(17, 19, 15, 3),

lwd = c(1.5, 2, 2, 2), bty = "n", cex = 0.85)

The Nelder-Mead simplex method (no derivatives) requires many more

function evaluations and takes a wandering path. BFGS with the AD

gradient converges more efficiently. nlminb() with both

gradient and Hessian can achieve the most direct path to the

optimum.

Summary

| What you need | Function | R optimizer argument |

|---|---|---|

| Gradient | gradient(f, x) |

gr in optim(), gradient in

nlminb()

|

| Hessian | hessian(f, x) |

hessian in nlminb() only |

| Observed information | -hessian(f, x) |

Post-optimization: invert for SEs |

When to use which optimizer:

-

optim()with BFGS — good default; usegr = function(x) -gradient(f, x) -

nlminb()— when you want second-order convergence; supply both gradient and Hessian - Nelder-Mead — fallback for non-smooth objectives; doesn’t benefit from AD

Remember the sign convention: optimizers minimize. For maximization, negate the function, gradient, and Hessian when passing to the optimizer.