When to Use This Package

Use compositional.mle when:

- Multi-modal likelihoods: Your likelihood surface has multiple local optima and you need global search strategies (simulated annealing, random restarts)

- Coarse-to-fine optimization: You want to start with a rough global search and progressively refine with local methods

- Comparing strategies: You’re unsure which optimizer works best and want to race them automatically

- Building robust pipelines: You need reliable estimation that handles edge cases gracefully

- Research/experimentation: You want to explore optimization strategies and visualize convergence

Stick with optim() when:

- You have a simple, well-behaved likelihood with a single optimum

- You know exactly which method works and don’t need composition

Example: Why Composition Matters

library(compositional.mle)

# A tricky bimodal likelihood

set.seed(42)

bimodal_loglike <- function(theta) {

# Two peaks: one at theta=2, one at theta=8

log(0.3 * dnorm(theta, 2, 0.5) + 0.7 * dnorm(theta, 8, 0.5))

}

problem <- mle_problem(

loglike = bimodal_loglike,

constraint = mle_constraint(support = function(theta) TRUE)

)

# Single gradient ascent gets trapped at local optimum

result_local <- gradient_ascent()(problem, theta0 = 0)

# Simulated annealing + gradient ascent finds global optimum

strategy <- sim_anneal(temp_init = 5, max_iter = 200) %>>% gradient_ascent()

result_global <- strategy(problem, theta0 = 0)

cat("Local search found:", round(result_local$theta.hat, 2),

"(log-lik:", round(result_local$loglike, 2), ")\n")

#> Local search found: 2 (log-lik: -1.43 )

cat("Global strategy found:", round(result_global$theta.hat, 2),

"(log-lik:", round(result_global$loglike, 2), ")\n")

#> Global strategy found: 2 (log-lik: -1.43 )Installation

# From CRAN (when available)

install.packages("compositional.mle")

# Development version

devtools::install_github("queelius/compositional.mle")Design Philosophy

Following SICP principles, the package provides: 1. Primitive solvers - gradient_ascent(), newton_raphson(), bfgs(), sim_anneal(), etc. 2. Composition operators - %>>% (sequential), %|% (race), with_restarts() 3. Closure property - Combining solvers yields a solver

Quick Start

# Generate sample data

set.seed(42)

x <- rnorm(100, mean = 5, sd = 2)

# Define the problem (separate from solver strategy)

problem <- mle_problem(

loglike = function(theta) {

if (theta[2] <= 0) return(-Inf)

sum(dnorm(x, theta[1], theta[2], log = TRUE))

},

score = function(theta) {

mu <- theta[1]; sigma <- theta[2]; n <- length(x)

c(sum(x - mu) / sigma^2,

-n / sigma + sum((x - mu)^2) / sigma^3)

},

constraint = mle_constraint(

support = function(theta) theta[2] > 0,

project = function(theta) c(theta[1], max(theta[2], 1e-8))

)

)

# Simple solve

result <- gradient_ascent()(problem, theta0 = c(0, 1))

result$theta.hat

#> [1] 5.065030 2.072274Composing Solvers

Sequential Chaining (%>>%)

Chain solvers for coarse-to-fine optimization:

# Grid search -> gradient ascent -> Newton-Raphson

strategy <- grid_search(lower = c(-10, 0.5), upper = c(10, 5), n = 5) %>>%

gradient_ascent(max_iter = 50) %>>%

newton_raphson(max_iter = 20)

result <- strategy(problem, theta0 = c(0, 1))

result$theta.hat

#> Var1 Var2

#> 5.065030 2.072274Parallel Racing (%|%)

Race multiple methods, keep the best:

# Try multiple approaches, pick winner by log-likelihood

strategy <- gradient_ascent() %|% bfgs() %|% nelder_mead()

result <- strategy(problem, theta0 = c(0, 1))

c(result$theta.hat, loglike = result$loglike)

#> loglike

#> 5.065030 2.072274 -214.758518Random Restarts

Escape local optima with multiple starting points:

strategy <- with_restarts(

gradient_ascent(),

n = 10,

sampler = uniform_sampler(c(-10, 0.5), c(10, 5))

)

result <- strategy(problem, theta0 = c(0, 1))

result$theta.hat

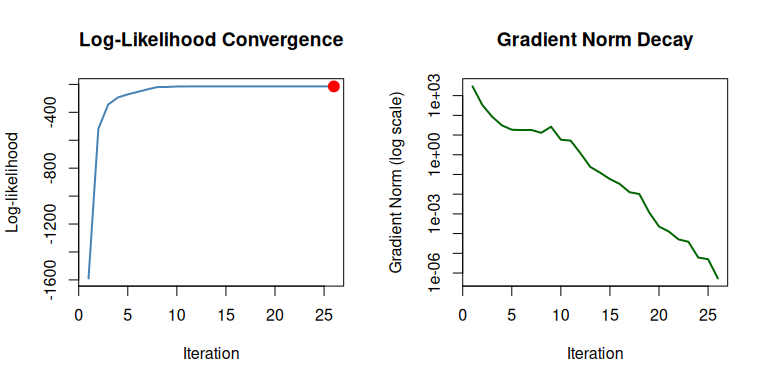

#> [1] 5.065030 2.072274Visualization

Track and visualize the optimization path:

# Enable tracing

trace_cfg <- mle_trace(values = TRUE, gradients = TRUE, path = TRUE)

result <- gradient_ascent(max_iter = 50)(problem, c(0, 1), trace = trace_cfg)

# Plot convergence

plot(result, which = c("loglike", "gradient"))

Extract trace as data frame for custom analysis:

path_df <- optimization_path(result)

head(path_df)

#> iteration loglike grad_norm theta_1 theta_2

#> 1 1 -1589.3361 2938.86063 0.0000000 1.000000

#> 2 2 -518.7066 334.47435 0.1723467 1.985036

#> 3 3 -344.5384 84.57555 0.5435804 2.913576

#> 4 4 -293.8366 30.83372 1.1733478 3.690360

#> 5 5 -271.7336 18.65296 2.1001220 4.065978

#> 6 6 -254.0618 17.83778 3.0615865 3.791049Available Solvers

| Factory | Method | Best For |

|---|---|---|

gradient_ascent() |

Steepest ascent with line search | General purpose, smooth likelihoods |

newton_raphson() |

Second-order Newton | Fast convergence near optimum |

bfgs() |

Quasi-Newton BFGS | Good balance of speed/robustness |

lbfgsb() |

L-BFGS-B with box constraints | High-dimensional, bounded parameters |

nelder_mead() |

Simplex (derivative-free) | Non-smooth or noisy likelihoods |

sim_anneal() |

Simulated annealing | Global optimization, multi-modal |

coordinate_ascent() |

One parameter at a time | Different parameter scales |

grid_search() |

Exhaustive grid | Finding starting points |

random_search() |

Random sampling | High-dimensional exploration |

Function Transformers

# Stochastic gradient (mini-batching for large data)

loglike_sgd <- with_subsampling(loglike, data = x, subsample_size = 32)

# Regularization

loglike_l2 <- with_penalty(loglike, penalty_l2(), lambda = 0.1)

loglike_l1 <- with_penalty(loglike, penalty_l1(), lambda = 0.1)Documentation

- Full documentation: https://queelius.github.io/compositional.mle/

- Vignettes: